ANZ owner-occupier loan book dips; NAB declines in investment housing arm

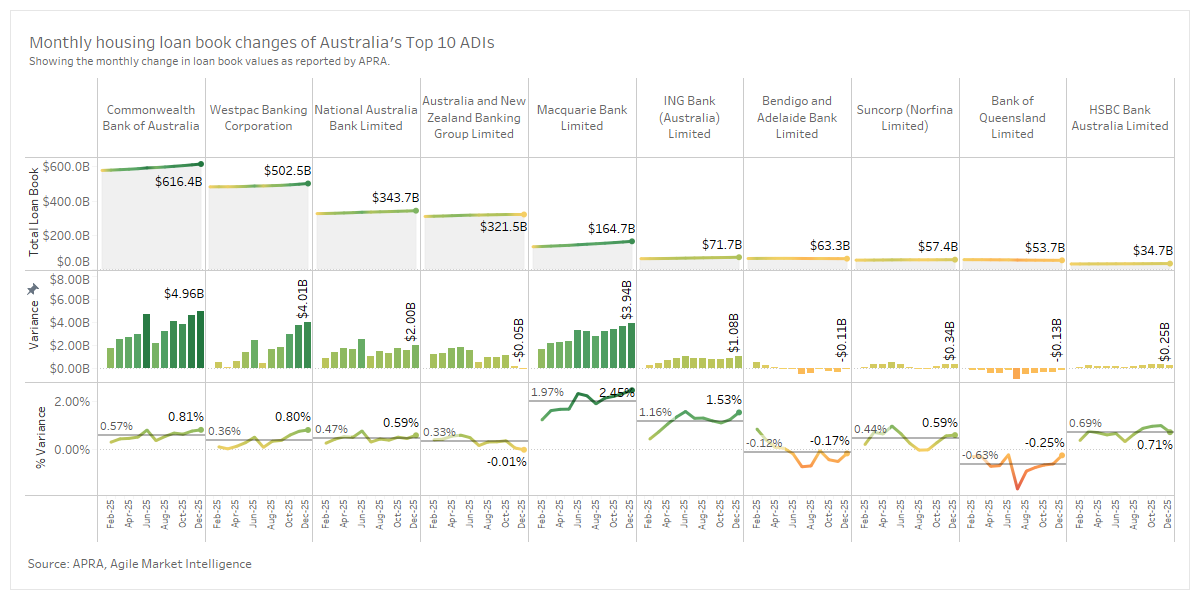

According to the Australian Prudential Regulation Authority (APRA), the top ten authorised deposit-taking institutions (ADIs) reached a combined $2.22 trillion loan book in December 2025. The total housing loan book combines owner-occupied housing loans and investment housing loans. Agile Market Intelligence plotted the publicly available APRA data of the total housing loan books, and broke it down to owner-occupied and investment housing loan books to visualise movements in the lending market. While banks such as Macquarie have gained as much as 2.45% month-on-month in December 2025, major banks ANZ and NAB saw parts of their housing loan books decrease towards the end of last year.

Key stats you need to know

- The top ten housing ADIs’ loan books accounted for $2.22 trillion out of the $2.43 trillion for all ADIs in December 2025.

- The Big 4 occupy 80% of the total housing loan book share.

- ANZ contracted in their owner-occupier arm, while NAB contracted in their investment segment.

In December 2025, the combined total housing loan book for all ADIs reached $2.43 trillion. A major slowdown was observed when loan book growth fell from 0.76% in June to 0.4% in July, but it has swiftly recovered momentum. The year ended with December seeing gains of $17.77 billion, a 0.74% growth rate from the previous month.

Macquarie's growth of 2.45% variance rate surpassed the Majors

- CBA had the biggest housing loan book at $616.4 billion, with the highest variance of $4.96 billion in December.

- Macquarie’s loan book grew 2.45% (amounting $3.94 billion), the highest across the board.

- ANZ, Bendigo and Adelaide, and BOQ are the only banks in the top ten to have contracted in December 2025.

CBA contributed most to the total housing loan book, with a variance of $4.96 billion (0.81%). This is followed by Westpac adding $4.01 billion (0.80% growth). Despite having a total loan book smaller than the rest of the Majors, Macquarie had the third-largest variance at $3.94B, and a variance rate of 2.45%, the highest across the board.

Surprisingly, ANZ’s housing loan book contracted by -0.01% (-$0.05 billion) despite the broader market’s trajectory. BOQ (-0.25%) and Bendigo (-0.17%) also saw their housing loan books contract by -$0.13 billion and -$0.11 billion, respectively.

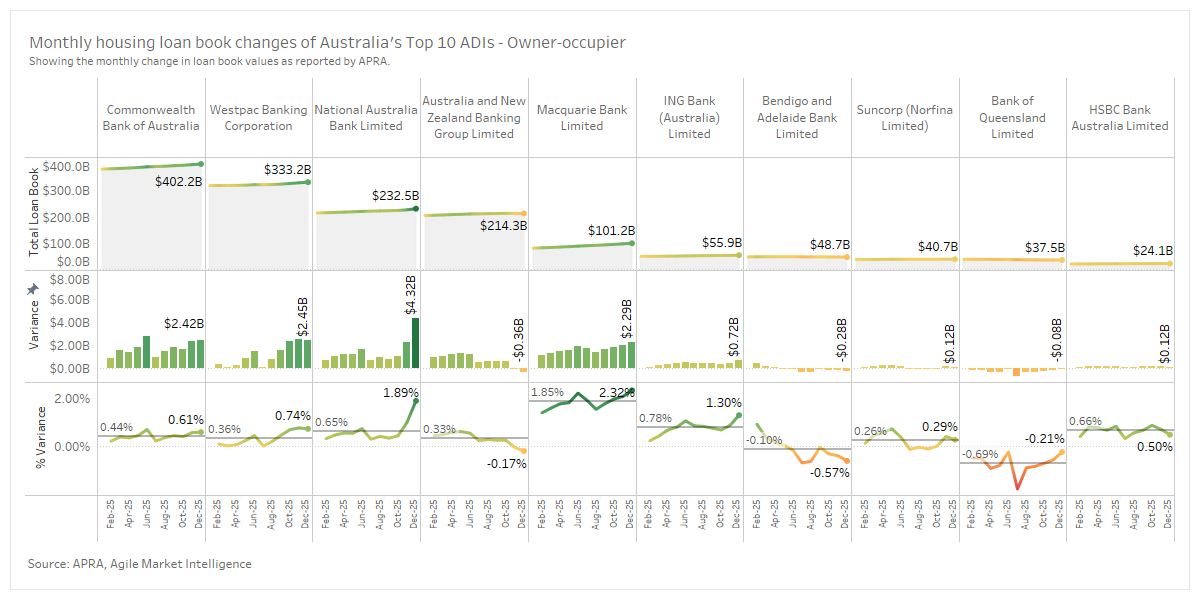

ANZ contracts by $0.36 billion in owner-occupier loans

- Owner-occupier loans ($1.64 trillion across all ADIs) make up two-thirds of the total housing loan books.

- Macquarie and NAB showed remarkable growth of 2.32% and 1.89%, respectively, in December.

- ANZ’s loan book contracted by -0.17%, equivalent to -$0.36 billion.

The overall contraction observed from ANZ stemmed from owner-occupier loans, a stark contrast to other major banks. CBA’s loan book grew by $2.42 billion, Westpac by $2.45, while NAB outpaced them all by a massive $4.32 billion growth. In terms of growth rate, however, Macquarie had the highest variance of +2.32%, with an equivalent value of $2.29 billion.

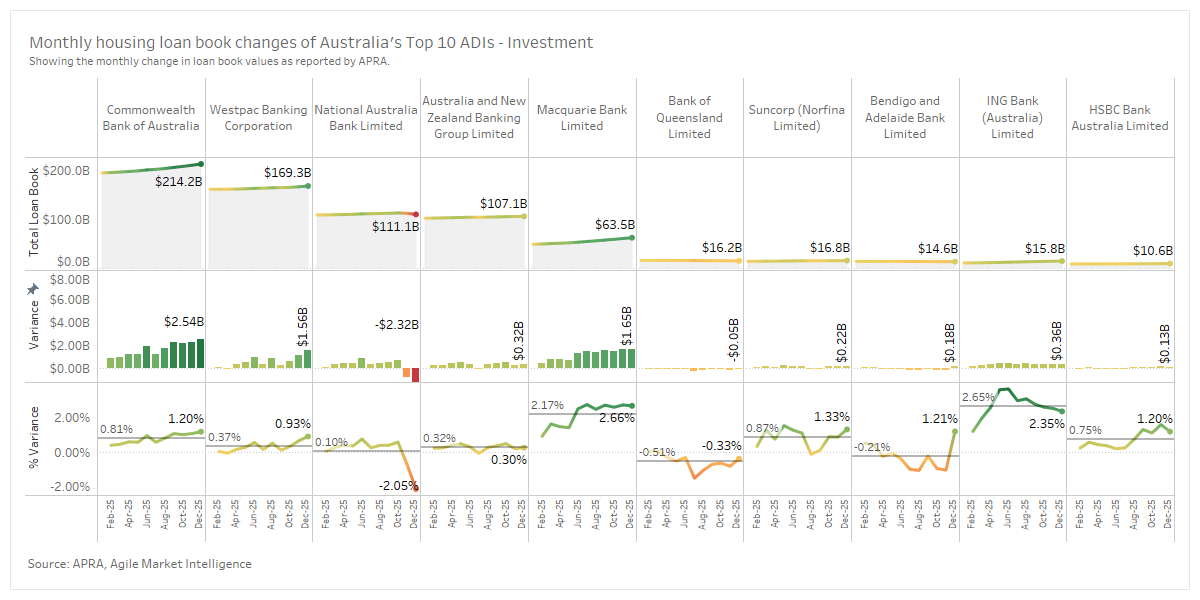

NAB investor loan book shrunk -$2.32 billion in December

- Total investment loan book for the top ten ADIs reached $739.2 billion in December 2025.

- NAB’s investment loan book contracted by -2.05%, equivalent to -$2.32 billion.

- Macquarie and ING demonstrated the highest growth of 2.66% and 2.35%, respectively.

While CBA’s investment loan book value grew the most in December ($2.45 billion), Macquarie comes in second, with $1.65 billion, beating Westpac’s $1.56 billion. Interestingly, despite having the third largest total loan book share, NAB’s investment loan book contracted by -2.05% (-$2.32 billion), despite its massive 1.89% positive growth for its owner-occupied loan book. ANZ holds steady with a 0.3% ($0.32 billion) growth, outpaced by ING’s $0.36 billion (+2.35%).

“In a time where Macquarie increased its loan book by 2.45%, and the system loan book has increased by 0.74%, contraction in ANZ’s owner-occupier loan book and NAB’s investment loan book are surprising," said Michael Johnson, Director at Agile Market Intelligence. “Banks are taking different approaches to balance growth and profitability in an increasingly competitive market.”

About the research

The figures in this article were drawn by Agile Market Intelligence from APRA’s monthly ADI statistics to December 2025. The dataset covers total housing loans segmented into owner-occupied and investment housing loans across the ten largest lenders by mortgage loan book size. For this analysis, Agile plotted publicly available data to show movements in loan books and market share.

Agile Market Intelligence also conducts Broker Pulse, a monthly survey of residential and commercial mortgage lenders. It is a community-driven knowledge base of lender performance that offers transparency to the market by surfacing these collective insights from the broker community. This empowers brokers to make informed decisions and enables lenders to benchmark and improve performance.

.svg%402x.png)

_100x30%403x.png)