One-third of owner-occupied lending in Q4 2025 considered ‘risky’

Australian Prudential Regulation Authority (APRA) has released its Quarterly ADI Property Exposure Statistics report for 2025 Q4 (December). Agile Market Intelligence has analysed and plotted the publicly available data and calculated the growth rates. The report shows that there has been an increase in risky loans in the last quarter of 2025, with a particular uptick for owner-occupied housing. With interest rates increasing this year, these numbers may be expected to rise.

Key stats you need to know

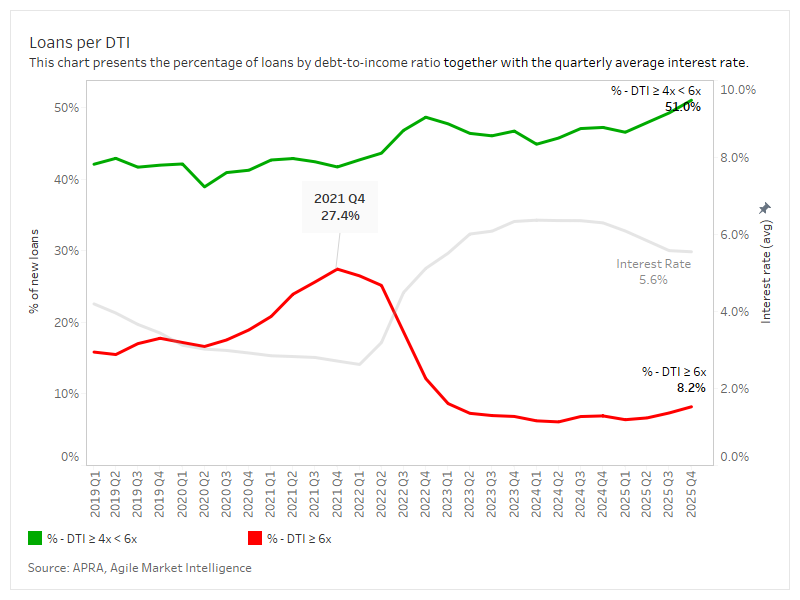

- The percentage of high-risk DTIs has risen to 8.2% in Q4 2025.

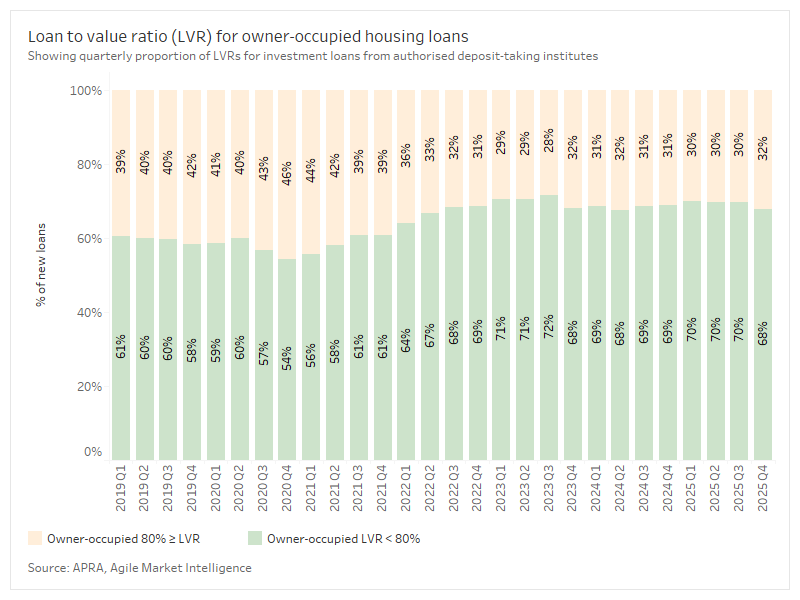

- Nearly 1 in 3 owner-occupied housing loans have a LVR exceeding 80%, thereby considered risky.

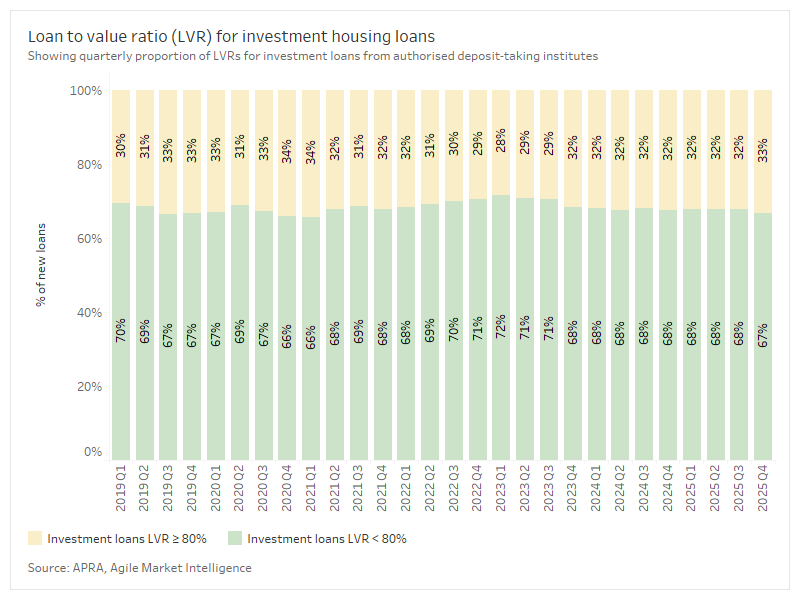

- LVR for investment housing loans remains steady at 33%.

High-risk DTIs ≥ 6x increased up to 8.2% in Q4 2025

- The average interest rate has remained at 5.6% at the end of 2025.

- The percentage of ‘safe’ DTI loans (less than 6x a borrower’s income) has increased to 51%.

Debt-to-income ratio (DTI) is a borrower’s credit limit across all debts in comparison to their gross income. The percentage of high-risk loans, DTI ≥ 6x, has increased from the previous quarter, landing at 8.2%. By contrast, safe loans are those whose DTI falls between 4 and 6 times a borrower’s income. As of December 2025, this percentage has risen to 51%.

“Seeing the rise of high-risk loans in the last quarter of 2025 is revealing of the risky appetite borrowers exhibited during the rate cuts last year,” said Michael Johnson, Director at Agile Market Intelligence. “It remains to be seen whether this risky appetite will continue to persist this year, after the RBA has hiked the cash rate twice already.”

High-risk housing loans increased up to 32%

Loan-to-value ratio (LTR) compares the amount of the mortgage in comparison to the asset being purchased. Those that fall below 80% indicate the borrower is a safe client, whereas loans exceeding this percentage are considered risky. The last quarter of 2025 has seen an uptick in risky loans for owner-occupied housing, having increased from 30% in Q3 to 32% in Q4. The LVR of investment housing loans maintains a steady appetite for risk, with a slight uptick by 1 percentage point last December.

About the research

Statistics in this article were drawn by Agile Market Intelligence from APRA’s quarterly ADI property exposure statistics (December 2025). The dataset covers property loans across authorised deposit-taking institutions, particularly loan-to-value statistics for owner-occupied and investment housing loans. Agile has plotted the loans per DTI together with the going average interest rate to show the proportion of high-risk loans.

Agile Market Intelligence also conducts Broker Pulse, a monthly survey of residential and commercial mortgage lenders. It is a community-driven knowledge base of lender performance that offers transparency to the market by surfacing these collective insights from the broker community. This empowers brokers to make informed decisions and enables lenders to benchmark and improve performance.

Participating brokers receive access to a bird’s-eye view of the lender benchmarking data each month. To sign up or for more information visit www.brokerpulse.com.au.

.svg%402x.png)

_100x30%403x.png)